Rsi TrendLines with Breakouts [KoTa]### RSI TrendLines with Breakouts Indicator: Detailed User Guide

The "RSI TrendLines with Breakouts " indicator is a custom Pine Script tool designed for TradingView. It builds on the standard Relative Strength Index (RSI) by adding dynamic trendlines based on RSI pivots (highs and lows) across multiple user-defined periods. These trendlines act as support and resistance levels on the RSI chart, and the indicator detects breakouts when the RSI crosses these lines, generating potential buy (long) or sell (short) signals. It also includes overbought/oversold thresholds and optional breakout labels. Below, I'll provide a detailed explanation in English, covering how to use it, its purpose, advantages and disadvantages, example strategies, and ways to enhance strategies with other indicators.

How to Use the Indicator

- The indicator uses `max_lines_count=500` to handle a large number of lines without performance issues, but on very long charts, you may need to zoom in for clarity.

1. **Customizing Settings**:

The indicator has several input groups for flexibility. Access them via the gear icon next to the indicator's name on the chart.

- **RSI Settings**:

- RSI Length: Default 14. This is the period for calculating the RSI. Shorter lengths (e.g., 7-10) make it more sensitive to recent price changes; longer (e.g., 20+) smooth it out for trends.

- RSI Source: Default is close price. You can change to open, high, low, or other sources like volume-weighted for different assets.

- Overbought Level: Default 70. RSI above this suggests potential overbuying.

- Oversold Level: Default 30. RSI below this suggests potential overselling.

- **Trend Periods**:

- You can enable/disable up to 5 periods (defaults: Period 1=3, Period 2=5, Period 3=10, Period 4=20, Period 5=50). Only enabled periods will draw trendlines.

- Each period detects pivots (highs/lows) in RSI using `ta.pivothigh` and `ta.pivotlow`. Shorter periods (e.g., 3-10) capture short-term trends; longer ones (20-50) show medium-to-long-term momentum.

- Inline checkboxes allow you to toggle display for each (e.g., display_p3=true by default).

- **Color Settings**:

- Resistance/Support Color: Defaults to red for resistance (up-trendlines from RSI highs) and green for support (down-trendlines from RSI lows).

- Labels for breakouts use green for "B" (buy/long) and red for "S" (sell/short).

- **Breakout Settings**:

- Show Prev. Breakouts: If true, displays previous breakout labels (up to "Max Prev. Breakouts Label" +1, default 2+1=3).

- Show Breakouts: Separate toggles for each period (e.g., show_breakouts3). When enabled, dotted extension lines project the trendline forward, and crossovers/crossunders trigger labels like "B3" (breakout above resistance for Period 3) or "S3" (break below support).

- Note: Divergence detection is commented out in the code. If you want to enable it, uncomment the relevant sections (e.g., show_divergence input) and adjust the lookback (default 5 bars) for spotting bullish/bearish divergences between price and RSI.

2. **Interpreting the Visuals**:

- **RSI Plot**: A blue line showing the RSI value (0-100). Horizontal dashed lines at 70 (red, overbought), 30 (green, oversold), and 50 (gray, midline).

- **Trendlines**: Solid lines connecting recent RSI pivots. Green lines (support) connect lows; red lines (resistance) connect highs. Only the most recent line per direction is shown per period to avoid clutter.

- **Breakout Projections**: Dotted lines extend the current trendline forward. When RSI crosses above a red dotted resistance, a "B" label (e.g., "B1") appears above, indicating a potential bullish breakout. Crossing below a green dotted support shows an "S" label below, indicating bearish.

- **Labels**: Current breakouts are bright (green/red); previous ones fade to gray. Use these as signal alerts.

- **Alerts**: The code includes commented-out alert conditions (e.g., for breakouts or RSI crossing levels). Uncomment and set them up in TradingView's alert menu for notifications.

3. **Best Practices**:

- Use on RSI-compatible timeframes (e.g., 1H, 4H, daily) for stocks, forex, or crypto.

- Combine with price chart: Trendlines are on RSI, so check if RSI breakouts align with price action (e.g., breaking a price resistance).

- Test on historical data: Backtest signals using TradingView's replay feature.

- Avoid over-customization initially—start with defaults (Periods 3 and 5 enabled) to understand behavior.

What It Is Used For

This indicator is primarily used for **momentum-based trend analysis and breakout trading on the RSI oscillator**. Traditional RSI identifies overbought/oversold conditions, but this enhances it by drawing dynamic trendlines on RSI itself, treating RSI as a "price-like" chart for trend detection.

- **Key Purposes**:

- **Identifying Momentum Trends**: RSI trendlines show if momentum is strengthening (upward-sloping support) or weakening (downward-sloping resistance), even if price is ranging.

- **Spotting Breakouts**: Detects when RSI breaks its own support/resistance, signaling potential price reversals or continuations. For example, an RSI breakout above resistance in an oversold zone might indicate a bullish price reversal.

- **Multi-Period Analysis**: By using multiple pivot periods, it acts like a multi-timeframe tool within RSI, helping confirm short-term signals with longer-term trends.

- **Signal Generation**: Breakout labels provide entry/exit points, especially in trending markets. It's useful for swing trading, scalping, or confirming trends in larger strategies.

- **Divergence (Optional)**: If enabled, it highlights mismatches between price highs/lows and RSI, which can predict reversals (e.g., bullish divergence: price lower low, RSI higher low).

Overall, it's ideal for traders who rely on oscillators but want more visual structure, like trendline traders applying price concepts to RSI.

Advantages and Disadvantages

**Advantages**:

- **Visual Clarity**: Trendlines make RSI easier to interpret than raw numbers, helping spot support/resistance in momentum without manual drawing.

- **Multi-Period Flexibility**: Multiple periods allow analyzing short- and long-term momentum simultaneously, reducing noise from single-period RSI.

- **Breakout Signals**: Automated detection of breakouts provides timely alerts, with labels and projections for proactive trading. This can improve entry timing in volatile markets.

- **Customization**: Extensive inputs (periods, colors, breakouts) make it adaptable to different assets/timeframes. The stateful management of lines/labels prevents chart clutter.

- **Complementary to Price Action**: Enhances standard RSI by adding trend context, useful for confirming divergences or overbought/oversold trades.

- **Efficiency**: Uses efficient arrays and line management, supporting up to 500 lines for long charts without lagging TradingView.

**Disadvantages**:

- **Lagging Nature**: Based on historical pivots, signals may lag in fast-moving markets, leading to late entries. Shorter periods help but increase whipsaws.

- **False Signals**: In ranging or sideways markets, RSI trendlines can produce frequent false breakouts. It performs better in trending conditions but may underperform without filters.

- **Over-Reliance on RSI**: Ignores volume, fundamentals, or price structure—breakouts might not translate to price moves if momentum decouples from price.

- **Complexity for Beginners**: Multiple periods and settings can overwhelm new users; misconfiguration (e.g., too many periods) leads to noisy charts.

- **No Built-in Risk Management**: Signals lack stop-loss/take-profit logic; users must add these manually.

- **Divergence Limitations**: The basic (commented) divergence detection is simplistic and may miss hidden divergences or require tuning.

In summary, it's powerful for momentum traders but should be used with confirmation tools to mitigate false positives.

Example Strategies

Here are one LONG (buy) and one SHORT (sell) strategy example using the indicator. These are basic; always backtest and use risk management (e.g., 1-2% risk per trade, stop-loss at recent lows/highs).

**LONG Strategy Example: Oversold RSI Support Breakout**

- **Setup**: Use on a daily chart for stocks or crypto. Enable Periods 3 and 5 (short- and medium-term). Set oversold level to 30.

- **Entry**: Wait for RSI to be in oversold (<30). Look for a "B" breakout label (e.g., "B3" or "B5") when RSI crosses above a red resistance trendline projection. Confirm with price forming a higher low or candlestick reversal (e.g., hammer).

- **Stop-Loss**: Place below the recent price low or the RSI support level equivalent in price terms (e.g., 5-10% below entry).

- **Take-Profit**: Target RSI reaching overbought (70) or a 2:1 risk-reward ratio. Exit on a bearish RSI crossunder midline (50).

- **Example Scenario**: In a downtrending stock, RSI hits 25 and forms a support trendline. On a "B5" breakout, enter long. This captures momentum reversals after overselling.

- **Rationale**: Breakout above RSI resistance in oversold signals fading selling pressure, potential for price uptrend.

**SHORT Strategy Example: Overbought RSI Resistance Breakout**

- **Setup**: Use on a 4H chart for forex pairs. Enable Periods 10 and 20. Set overbought level to 70.

- **Entry**: Wait for RSI in overbought (>70). Enter on an "S" breakout label (e.g., "S3" or "S4") when RSI crosses below a green support trendline projection. Confirm with price showing a lower high or bearish candlestick (e.g., shooting star).

- **Stop-Loss**: Above the recent price high or RSI resistance level (e.g., 5-10% above entry).

- **Take-Profit**: Target RSI hitting oversold (30) or a 2:1 risk-reward. Exit on bullish RSI crossover midline (50).

- **Example Scenario**: In an uptrending pair, RSI peaks at 75 with a resistance trendline. On "S4" breakout, enter short. This targets momentum exhaustion after overbuying.

- **Rationale**: Break below RSI support in overbought indicates weakening buying momentum, likely price downturn.

Enhancing Strategy Validity with Other Indicators

To increase the reliability of strategies based on this indicator, combine it with complementary tools for confirmation, filtering false signals, and adding context. This creates multi-indicator strategies that reduce whipsaws and improve win rates. Focus on indicators that address RSI's weaknesses (e.g., lagging, momentum-only). Below are examples of different indicators, how to integrate them, and sample strategies.

1. **Moving Averages (e.g., SMA/EMA)**:

- **How to Use**: Overlay 50/200-period EMAs on the price chart. Use RSI breakouts only in the direction of the trend (e.g., long only if price > 200 EMA).

- **Strategy Example**: Trend-Following Long – Enter on "B" RSI breakout if price is above 200 EMA and RSI > 50. This filters reversals in uptrends. Add MACD crossover for entry timing. Advantage: Aligns momentum with price trend, reducing counter-trend trades.

2. **Volume Indicators (e.g., Volume Oscillator or OBV)**:

- **How to Use**: Require increasing volume on RSI breakouts (e.g., OBV making higher highs on bullish breakouts).

- **Strategy Example**: Volume-Confirmed Short – On "S" breakout, check if volume is rising and OBV breaks its own trendline downward. Enter short only if confirmed. This validates breakouts with real market participation, avoiding low-volume traps.

3. **Other Oscillators (e.g., MACD or Stochastic)**:

- **How to Use**: Use for divergence confirmation or overbought/oversold alignment. For instance, require Stochastic (14,3,3) to also breakout from its levels.

- **Strategy Example**: Dual-Oscillator Reversal Long – Enable divergence in the indicator. Enter on bullish RSI divergence + "B" breakout if MACD histogram flips positive. Exit on MACD bearish crossover. This strengthens reversal signals by cross-verifying momentum.

4. **Price Action Tools (e.g., Support/Resistance or Candlestick Patterns)**:

- **How to Use**: Map RSI trendlines to price levels (e.g., if RSI resistance breaks, check if price breaks a key resistance).

- **Strategy Example**: Price-Aligned Breakout Short – On "S" RSI breakout in overbought, confirm with price breaking below a drawn support line or forming a bearish engulfing candle. Use Fibonacci retracements for targets. This ensures momentum translates to price movement.

5. **Volatility Indicators (e.g., Bollinger Bands or ATR)**:

- **How to Use**: Avoid trades during low volatility (e.g., Bollinger Band squeeze) to filter ranging markets. Use ATR for dynamic stops.

- **Strategy Example**: Volatility-Filtered Long – Enter "B" breakout only if Bollinger Bands are expanding (increasing volatility) and RSI is oversold. Set stop-loss at 1.5x ATR below entry. This targets high-momentum breakouts while skipping choppy periods.

**General Tips for Building Enhanced Strategies**:

- **Layering**: Start with RSI breakout as the primary signal, add 1-2 confirmations (e.g., EMA trend + volume).

- **Backtesting**: Use TradingView's strategy tester to quantify win rates with/without additions.

- **Risk Filters**: Incorporate overall market sentiment (e.g., via VIX) or avoid trading near news events.

- **Timeframe Alignment**: Use higher timeframes for trend (e.g., daily EMA) and lower for entries (e.g., 1H RSI breakout).

- **Avoid Overloading**: Too many indicators cause paralysis; aim for synergy (e.g., trend + momentum + volume).

This indicator is a versatile tool, but success depends on context and discipline. If you need code modifications or specific backtests, provide more details!

스크립트에서 "high low"에 대해 찾기

Trend lines indicator by ForexBeeEnhanced 3-Swing Trendline Zones - Complete Feature Guide

WHAT THIS INDICATOR DOES

This indicator automatically draws trendline zones on your chart using a 3-point validation system. Instead of just connecting any two price points like basic trendline tools, it waits for three swing points to confirm the trendline is valid before drawing it.

FEATURE 1: SWING POINT DETECTION

What it detects:

Swing highs: Price points where the high is higher than surrounding candles

Swing lows: Price points where the low is lower than surrounding candles

These show up as small arrows on your chart labeled "SH" (swing high) and "SL" (swing low)

Settings that control this:

Swing Length : Default is 6, range 1-20

Higher numbers = fewer, more significant swing points

Lower numbers = more swing points, including minor ones

Example: Setting 5 means each swing point must be higher/lower than 5 candles on each side

How to use this setting:

On 1-minute charts: Use 5-10 to filter out noise

On daily charts: Use 2-3 for more sensitivity

Volatile markets: Increase the number

Quiet markets: Decrease the number

Please See the Below Images To See the difference of swing length of 6 and 8

Display control:

Show Swing Points : Turn the arrows on/off

Default: ON (you'll see the arrows)

Turn OFF if arrows clutter your chart

FEATURE 2: RETRACEMENT VALIDATION SYSTEM

What this does:

After finding two swing points, the system checks if the second swing represents a proper market retracement, not just random price movement.

How it works:

Finds the highest point between two swing lows (or lowest point between two swing highs)

Calculates how much the second swing retraced from this extreme point

Only accepts swings that retrace between your set percentages

Settings that control this:

Lower Limit % : Default 50%, range 0-100%

Upper Limit % : Default 90%, range 0-100%

These create a "valid retracement zone"

Why this matters:

Eliminates random trendlines that don't follow market structure

Ensures trendlines represent actual retracement patterns

Based on Elliott Wave and Fibonacci principles

FEATURE 3: ATR-BASED ZONE WIDTH

What ATR means:

Average True Range measures how much price typically moves in a given period. Instead of fixed-width trendlines, this creates zones that adapt to market volatility.

Settings that control this:

Zone Width (ATR Multiple) : Default 0.3, range 0.1-1.0

ATR Length : Default 14, range 1-50 periods

How zone width works:

Multiplier 0.1 = Very narrow zones (tight around trendline)

Multiplier 0.5 = Medium zones

Multiplier 1.0 = Wide zones (accommodates more price movement)

ATR Length explained:

14 periods = Uses last 14 candles to calculate average volatility

Shorter periods (7) = More sensitive to recent volatility changes

Longer periods (21) = Smoother, less sensitive to volatility spikes

Practical impact:

During high volatility: Zones automatically become wider

During low volatility: Zones automatically become narrower

Prevents false breakouts during normal market noise

Creates realistic support/resistance areas instead of precise lines

FEATURE 4: VISUAL ZONE SYSTEM

Active Uptrend Zones:

Green upper boundary line (solid, thick)

Lime green lower boundary line (solid, thick)

Green fill between lines (80% transparency)

These represent dynamic support levels

Active Downtrend Zones:

Blue upper boundary line (solid, thick)

Navy blue lower boundary line (solid, thick)

Red fill between lines (80% transparency)

These represent dynamic resistance levels

Broken/Expired Zones:

Gray/silver boundary lines (dashed, thick)

Original fill color maintained (green for uptrend zones, red for downtrend zones)

Shows historical trendlines that are no longer active

FEATURE 5: BREAK DETECTION SYSTEM

How breaks are detected:

The system monitors when price violates the zone boundaries, indicating the trendline structure has failed.

Settings that control this:

Use Wick Break : True/False toggle

TRUE: Break occurs when candle high/low touches zone boundary

FALSE: Break occurs when candle close price crosses zone boundary

Conservative vs Aggressive approach:

Wick Break = TRUE (Aggressive) :

- More sensitive, earlier signals

- May produce more false breaks during volatile periods

- Good for scalping and short-term trading

Wick Break = FALSE (Conservative) :

- Requires candle to close beyond zone

- Fewer false signals, more reliable breaks

- Better for swing trading and position trading

What happens when zone breaks:

Zone lines change from solid to dashed

Zone lines change color to gray/silver

Fill color remains original (green/red) for identification

Zone stops extending forward

Zone is removed from active monitoring

FEATURE 6: ZONE EXPIRATION SYSTEM

What expiration does:

Allows trendlines to automatically become inactive after a set number of bars, even if they haven't been broken.

Settings that control this:

Use Zone Expiration : True/False toggle

Zone Expiration (Bars) : Default 500, range 1-1000

FALSE: Zones run indefinitely until broken

TRUE: Zones expire after specified number of bars

Visual result:

Expired zones look identical to broken zones

Lines become dashed and gray/silver

Fill colors remain original (green/red)

FEATURE 7: MULTI-TIMEFRAME TREND ANALYSIS TABLE

What the table shows:

A small table on your chart that monitors trend conditions across four different timeframes simultaneously.

Settings that control this:

TF1, TF2, TF3, TF4 : Four customizable timeframes

Default: 4H, 8H, 1D, 1W

Table Position : 9 positions (top/middle/bottom + left/center/right)

Text Size : Tiny, Small, Normal, Large, Huge

How trend detection works:

Uptrend Pattern : Current candle's high AND low are both higher than previous candle's high AND low on specified timeframes

This creates higher highs and higher lows

Shows consistent buying pressure

Table displays green background with upward arrow (▲)

Downtrend Pattern : Current candle's high AND low are both lower than previous candle's high AND low on specified timeframes

This creates lower highs and lower lows

Shows consistent selling pressure

Table displays red background with downward arrow (▼)

Range/Sideways Pattern : Current candle creates either inside bar or outside bar

Inside bar: Current range smaller than previous candle

Outside bar: Current range larger than previous candle

Shows market indecision or consolidation

Table displays orange background with diamond symbol (◆)

No Clear Pattern : None of the above conditions are met

Table displays gray background with horizontal line (⎯)

How to interpret the table:

All timeframes green (uptrend): Strong bullish alignment

All timeframes red (downtrend): Strong bearish alignment

Mixed colors: Conflicting timeframes, exercise caution

Mostly orange: Market in consolidation phase

Tooltip explanations: Hover over each cell for detailed description

FEATURE 8: BACKGROUND COLOR SYSTEM

What background colors show:

Optional feature that colors your chart background based on the current timeframe's trend condition.

Settings that control this:

Show Background Colors : True/False toggle

Background Transparency : 80-98% range

Default: OFF (no background colors)

Color scheme:

Green background: Current timeframe showing uptrend

Red background: Current timeframe showing downtrend

Orange background: Current timeframe showing range/consolidation

No background: No clear trend pattern

Transparency levels:

80%: More visible background color

95%: Subtle background hint

98%: Very subtle background tint

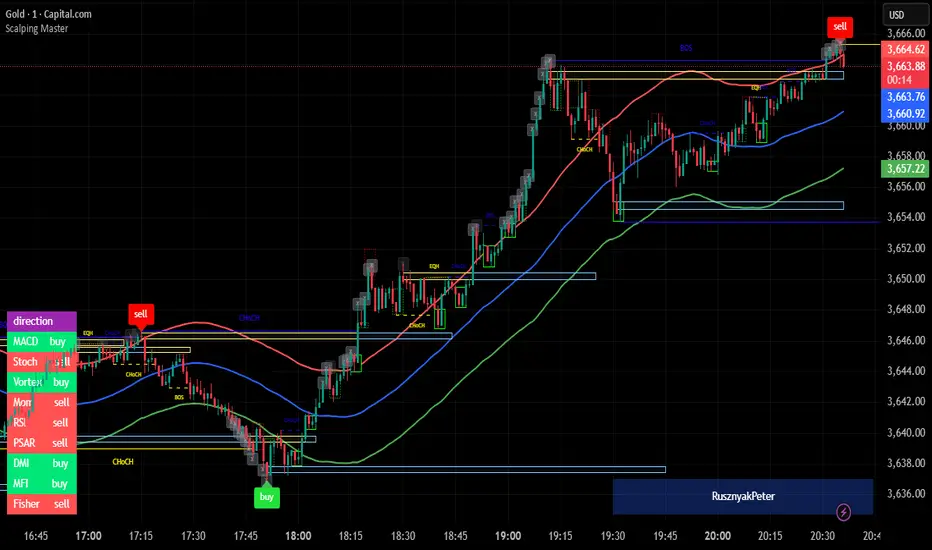

Scalping MasterMarket Structure Analysis:

Swing Structure: Detects higher highs (HH), lower highs (LH), higher lows (HL), aur lower lows (LL) ko identify karta hai using pivot points (based on ta.highest aur ta.lowest).

Internal Structure: Chhote timeframes ke liye internal swing points aur break of structure (BOS)/change of character (CHoCH) ko track karta hai.

BOS/CHoCH Detection: Bullish aur bearish structure breaks (BOS) aur trend reversals (CHoCH) ko label karta hai.

Order Blocks (OB):

Internal Order Blocks: Chhote timeframe ke order blocks ko plot karta hai, jo liquidity zones ko represent karte hain.

Swing Order Blocks: Bade timeframe ke order blocks ko show karta hai.

Filtering: ATR ya Cumulative Mean Range ke basis par volatile order blocks ko filter karta hai.

Fair Value Gaps (FVG):

Price gaps (bullish aur bearish) ko detect aur plot karta hai.

Auto-threshold aur timeframe customization ke saath FVGs ko filter karta hai.

FVGs ko extend karne ka option deta hai (visual representation ke liye).

Equal Highs/Lows (EQH/EQL):

Equal highs aur lows ko identify karta hai, jo support/resistance zones ke liye useful hote hain.

Bars confirmation aur sensitivity threshold ke saath customizable hai.

Previous Highs/Lows (MTF):

Daily, weekly, aur monthly high/low levels ko plot karta hai.

Line style (solid, dashed, dotted) aur colors customizable hain.

Premium/Discount Zones:

Market ke premium, equilibrium, aur discount zones ko highlight karta hai, jo price action ke liye key areas hote hain.

Visual Customization:

Color Themes: Colored ya monochrome themes ke options.

Candle Coloring: Trend ke hisaab se candles ko color karta hai.

Labels aur Lines: Swing points, strong/weak highs/lows, aur structure breaks ke liye labels aur lines plot karta hai.

Modes:

Historical Mode: Past data ke saath complete structure dikhata hai.

Present Mode: Sirf recent structure aur signals dikhata hai, clutter reduce karne ke liye.

Alerts:

Bullish/Bearish BOS, CHoCH, order block breaks, aur EQH/EQL ke liye alerts set karne ka option.

Swing Points aur Trailing:

Strong/weak high aur low points ko track karta hai.

Trailing maximum/minimum ko extend karta hai for real-time analysis.

Kya Kya Mila Kar Bana Hai?

Yeh indicator Smart Money Concepts ke core principles par based hai aur in elements ko combine karta hai:

Pivot Point Analysis:

ta.highest aur ta.lowest functions se swing highs/lows detect karta hai.

Internal aur swing structure ke liye alag-alag lengths (e.g., length aur 5 for internal swings).

Price Action Concepts:

Break of Structure (BOS): Jab price pivot high/low ko break karta hai.

Change of Character (CHoCH): Jab trend reverse hota hai.

Confluence filtering ke saath accuracy improve karta hai.

Order Blocks:

Liquidity zones ko identify karne ke liye high/low ranges aur ATR/cumulative mean range ka use.

Bullish aur bearish order blocks ke liye customizable colors.

Fair Value Gaps:

Gaps in price action ko detect karne ke liye OHLC data ka analysis.

Timeframe aur auto-threshold ke saath flexibility.

MTF (Multi-Timeframe) Analysis:

Daily, weekly, monthly high/low levels ke liye ta.valuewhen aur time-based calculations.

Zones Detection:

Premium, equilibrium, aur discount zones ke liye price range calculations.

Visual Tools:

Lines, labels, aur boxes ke saath market structure ko visually represent karta hai (line.new, label.new, box.new).

Extendable lines aur boxes for better visibility.

User Inputs:

Customizable settings jaise timeframe, colors, lengths, aur filters, jo user ko flexibility dete hain.

Technical Components

PineScript Functions: ta.crossover, ta.crossunder, ta.highest, ta.lowest, ta.atr, ta.cum for calculations.

Arrays: Order blocks ke coordinates store karne ke liye (array.new_float, array.new_int, array.new_box).

Drawing Tools: Lines, labels, aur boxes ke saath dynamic plotting.

Conditional Logic: BOS, CHoCH, aur other signals ke liye complex conditions.

Timeframe Support: Multi-timeframe analysis ke liye input.timeframe.

Key Levels: Daily, Weekly, Monthly [BackQuant]Key Levels: Daily, Weekly, Monthly

Map the market’s “memory” in one glance—yesterday’s range, this week’s chosen day high/low, and D/W/M opens—then auto-clean levels once they break.

What it does

This tool plots three families of high-signal reference lines and keeps them tidy as price evolves:

Chosen Day High/Low (per week) — Pick a weekday (e.g., Monday). For each past week, the script records that day’s session high and low and projects them forward for a configurable number of bars. These act like “memory levels” that price often revisits.

Daily / Weekly / Monthly Opens — Plots the opening price of each new day, week, and month with separate styling. These opens frequently behave like magnets/flip lines intraday and anchors for regime on higher timeframes.

Auto-pruning — When price breaks a stored level, the script can automatically remove it to reduce clutter and refocus you on still-active lines. See: (broken levels removed).

Why these levels matter

Liquidity pockets — Prior day’s high/low and the daily open concentrate stops and pending orders. Mapping them quickly reveals likely sweep or fade zones. Example: previous day highs + daily open highlighting liquidity:

Context & regime — Monthly opens frame macro bias; trading above a rising cluster of monthly opens vs. below gives a clean top-down read. Example: monthly-only “macro outlook” view:

Cleaner charts — Auto-remove broken lines so you focus on what still matters right now.

What it plots (at a glance)

Past Chosen Day High/Low for up to N prior weeks (your choice), extended right.

Current Daily Open , Weekly Open , and Monthly Open , each with its own color, label, and forward extension.

Optional short labels (e.g., “Mon High”) or full labels (with week/month info).

How breaks are detected & cleaned

You control both the evidence and the timing of a “break”:

Break uses — Choose Close (more conservative) or Wick (more sensitive).

Inclusive? — If enabled, equality counts (≥ high or ≤ low). If disabled, you need a strict cross.

Allow intraday breaks? — If on, a level can break during the tracked day; if off, the script only counts breaks after the session completes.

Remove Broken Levels — When a break is confirmed, the line/label is deleted automatically. (See the demo: )

Quick start

Pick a Day of Week to Track (e.g., Monday).

Set how many weeks back to show (e.g., 8–10).

Choose how far to extend each family (bars to the right for chosen-day H/L and D/W/M opens).

Decide if a break uses Close or Wick , and whether equality counts.

Toggle Remove Broken Levels to keep the chart clean automatically.

Tips by use-case

Intraday bias — Watch the Daily Open as a magnet/flip. If price gaps above and holds, pullbacks to the daily open often decide direction. Pair with last day’s high/low for sweep→reversal or true breakout cues. See:

Weekly structure — Track the week’s chosen day (e.g., Monday) high/low across prior weeks. If price stalls near a cluster of old “Monday Highs,” look for sweep/reject patterns or continuation on reclaim.

Macro regime — Hide daily/weekly lines and keep only Monthly Opens to read bigger cycles at a glance (BTC/crypto especially). Example:

Customization

Use wicks or bodies for highs/lows (wicks capture extremes; bodies are stricter).

Line style & thickness — solid/dashed/dotted, width 1–5, plus global transparency.

Labels — Abbreviated (“Mon High”, “D Open”) or full (month/week/day info).

Color scheme — Separate colors for highs, lows, and each of D/W/M opens.

Capacity controls — Set how many daily/weekly/monthly opens and how many weeks of chosen-day H/L to keep visible.

What’s under the hood

On your selected weekday, the script records that session’s true high and true low (using wicks or body-based extremes—your choice), then projects a horizontal line forward for the next bars.

At each new day/week/month , it records the opening price and projects that line forward as well.

Each bar, the script checks your “break” rules; once broken, lines/labels are removed if auto-cleaning is on.

Everything updates in real time; past levels don’t repaint after the session finishes.

Recommended presets

Day trading — Weeks back: 6–10; extend D/W opens: 50–100 bars; Break uses: Close ; Inclusive: off; Auto-remove: on.

Swing — Fewer daily opens, more weekly opens (2–6), and 8–12 weeks of chosen-day H/L.

Macro — Show only Monthly Opens (1–6 months), dashed style, thicker lines for clarity.

Reading the examples

Broken lines disappear — decluttering in action:

Macro outlook — monthly opens as cycle rails:

Liquidity map — previous day highs + daily open:

Final note

These are not “signals”—they’re reference points that many participants watch. By standardising how you draw them and automatically clearing the ones that no longer matter, you turn a noisy chart into a focused map: where liquidity likely sits, where price memory lives, and which lines are still in play.

Multi-Timeframe SMTSummery

The Multi-Timeframe SMT indicator is designed to identify and visualize Higher Timeframe (HTF) data on a Lower Timeframe (LTF) chart, allowing traders to see the broader market context without changing their current chart's resolution. It accurately draws pivots and SMT divergences from higher timeframes on the corresponding candles of your current lower timeframe chart.

Its core features include:

Multi-Timeframe Analysis: Configure and monitor pivots on up to four independent timeframes, from intraday to monthly.

Customizable Pivot Detection: Define the strength of pivots by adjusting the number of bars to the left and right.

SMT Divergence: Automatically identifies bullish and bearish SMT divergences by comparing the price action of the main chart symbol with a chosen correlated asset.

Early SMT Detection: A unique feature that monitors a lower "detection timeframe" to provide early warnings of potential SMT setups before they're confirmed on the main timeframe. Note that this early detection is only shown on timeframes equal to or lower than the "Detection timeframe" you have set.

Visual Cues & Alerts: Clear on-chart labels, lines, and fully customizable alerts notify you of confirmed pivots and SMT divergences, ensuring you don't miss key opportunities.

Important Nuance Regarding Pivot Label Display

Due to a self-imposed limit within this script's drawing management logic, the indicator might quickly reach its drawing capacity if you enable pivot crosses for multiple timeframes simultaneously. When this internal drawing limit is exceeded, the script is designed to automatically remove the oldest drawings to make space for new ones.

Therefore, to ensure optimal performance and visibility of the most recent and relevant pivots, it's highly recommended to only enable the "Show Pivot Crosses" option for one timeframe at a time. If you wish to view pivots for a different timeframe, simply disable the pivot crosses for the currently active timeframe and then enable them for your desired one. This approach prevents the rapid cycling and disappearance of pivot labels, providing a clearer and more stable visual experience.

In-Depth Explanation of the Logic

This script is built on two primary concepts: pivot points and Smart Money Technique (SMT) divergence. It systematically collects historical data on multiple timeframes, identifies pivots, and then compares them between two assets to find divergences.

Pivot Point Identification

A pivot is a turning point in the market. A pivot high is a candle that has a higher high than the candles to its immediate left and right. Conversely, a pivot low is a candle with a lower low than its neighbors.

How it Works in the Script:

The script tracks the highest high and lowest low for each period of the selected timeframe (e.g., for each 4-hour candle). When a new high-timeframe candle closes, it stores that high/low value and its bar index in an array. The checkForPivot() function then checks if a recently stored high or low qualifies as a pivot.

Key Inputs:

Left Strength (leftBars1): The number of candles to the left that must have a lower high (for a pivot high) or higher low (for a pivot low).

Right Strength (rightBars1): The number of candles to the right that must meet the same criteria.

For example, with Left Strength and Right Strength both set to 3, a pivot high is only confirmed when its high is greater than the highs of the 3 previous high-timeframe candles and the 3 subsequent high-timeframe candles. Increasing these values will identify more significant, longer-term pivots.

Smart Money Technique (SMT) Divergence

SMT Divergence is a concept popularized by The Inner Circle Trader (ICT). It occurs when two closely correlated assets fail to move in sync. For instance, if Asset A makes a higher high but Asset B fails to do so and instead makes a lower high, this creates a bearish SMT divergence. It suggests that the "smart money" may not be supporting the move in Asset A, signaling a potential reversal.

Bearish SMT: Main asset makes a higher high, while the correlated asset makes a lower high. This is a potential sell signal.

Bullish SMT: Main asset makes a lower low, while the correlated asset makes a higher low. This is a potential buy signal.

How it Works in the Script:

Data Request: For each timeframe, the script uses the request.security() function to fetch the high and low data for both the main chart symbol (syminfo.tickerid) and the chosen Comparison Asset.

Pivot Comparison: When a new pivot is confirmed on the main asset, the script checks if a corresponding pivot also formed on the comparison asset at the same time.

Divergence Check: It then compares the direction of the pivots. For a bearish SMT, it checks if the main asset's new pivot high is higher than its previous pivot high, while the comparison asset's new pivot high is lower than its previous one. The logic is reversed for bullish SMT.

Visualization: If a divergence is found, the script draws a red (bearish) or green (bullish) line connecting the two pivots on your chart and places an "SMT" label.

Early SMT Detection

This is a proactive feature designed to give you a heads-up. Waiting for a 4-hour or daily pivot to form can take a long time. The early detection system looks for SMT divergences on a much smaller, user-defined Detection timeframe (e.g., 15-minute).

How it Works in the Script:

Awaiting Setup: After a primary pivot (Pivot A) is formed on the main timeframe (e.g., a Daily pivot high), the script begins monitoring.

Intraday Monitoring: It then watches the Detection timeframe (e.g., 15-minute) for smaller intraday pivots.

Potential Divergence: It looks for an intraday pivot that forms a divergence against the primary Pivot A.

Watchline & Alert: When this "potential" divergence occurs, the script draws a dashed white line and triggers a "Potential SMT" alert. This isn't a confirmed SMT on the main timeframe yet, but it's a powerful early warning that one may be forming.

Drawing & Object Management

To keep the chart clean and prevent performance issues, the script manages its drawings (lines and labels) efficiently. It stores them in arrays and uses a drawing limit to automatically delete the oldest drawings as new ones are created, ensuring your TradingView remains responsive.

How to Use the Indicator

Configuration

Enable Timeframes: Use the checkboxes (Enable Timeframe 1, Enable Timeframe 2, etc.) to activate the timeframes you want to monitor. It's often best to start with one or two to keep the chart clean.

Select Timeframes: Choose the higher timeframes you want to analyze (e.g., 240 for 4-hour, D for Daily, W for Weekly).

Set Pivot Strength: The default of 3 for Left/Right strength is a good starting point. Increase it to find more significant market structure points or decrease it for more frequent, shorter-term pivots.

Configure SMT:

Check Enable SMT for the timeframes where you want to detect divergence.

Enter a Comparison Asset . This is crucial. Ensure the assets are correlated.

To use the early warning system, check Enable early SMT detection and select an appropriate Detection timeframe (e.g., 15 or 60 minutes for a Daily analysis).

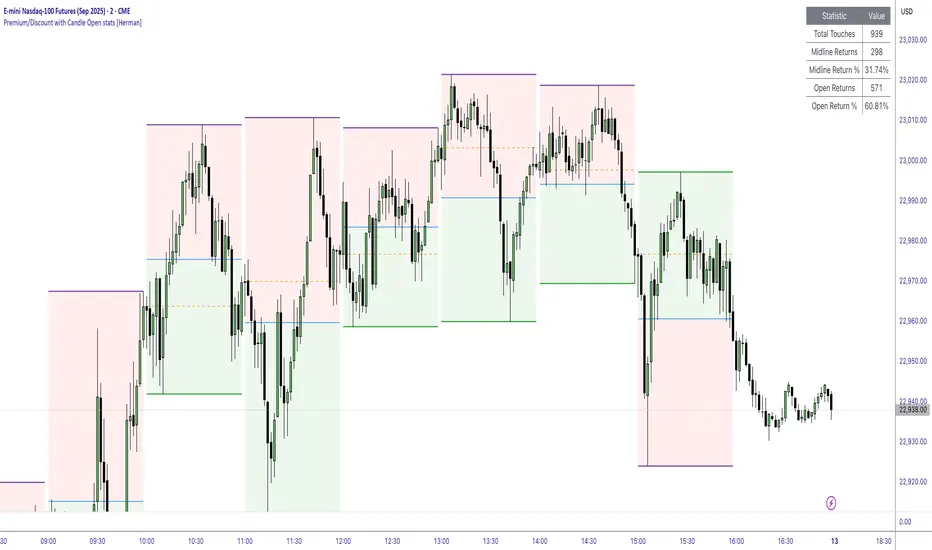

Premium/Discount with Candle Open stats [Herman]Premium/Discount with Stats

This indicator is designed to help traders identify and analyze premium/discount zones on any timeframe while automatically tracking statistics on price behavior relative to these zones. It is especially valuable for traders looking to structure entries, manage targets, and quantify market reactions to prior session ranges.

What it draws on the chart

✅ Range High and Low Lines

For each selected timeframe period (15min, 30min 1H, 4H, Daily), the indicator plots the high and low of the completed previous period.

These lines are color-coded dynamically based on sweep detection:

If the high was swept (price broke the previous high), the high line is marked as Premium.

If the low was swept, the low line is marked as Discount.

If both were swept or neither, it uses the default color settings.

✅ Midline

An optional midline at the 50% level of the previous period’s high-low range.

Helpful for mean-reversion traders or anyone watching for retests of equilibrium.

✅ Quartile Lines (25%–75%)

Optional additional lines at 25% and 75% of the previous range, helping traders visualize inner range subdivisions.

✅ Open Price Line

Marks the open price of the previous period as a horizontal reference.

✅ Background Fills

The region between low and midline is shaded with the Discount color.

The region between high and midline is shaded with the Premium color.

These optional fills help highlight the premium and discount zones visually.

✅ Current Incomplete Period Lines (optional)

You can choose to display provisional high, low, midline, quartiles, and open for the current forming period.

These update in real-time until the period closes.

Sweep Detection Logic

The indicator automatically tracks if the current period price sweeps above the previous period’s high or below the low.

A "sweep" is simply defined as price exceeding the previous high/low while tracking is active.

The sweep status affects the colors of the premium/discount lines, helping traders see potential liquidity grabs or stop hunts.

What it counts and tracks (Statistics)

The script automatically compiles statistics over time:

✅ Total Touches

Counts how many times the price in a new period touches either the previous period’s high or low.

A “touch” is registered once per side per period.

✅ Midline Returns

Counts how often, after touching the previous high/low, price returns to the previous period’s midline.

Gives you a measure of mean-reversion success.

✅ Open Returns

Similarly, tracks how often price returns to the previous period’s open after touching the previous high/low.

✅ Return Percentages

Displays the percentage of touches that result in a return to midline or open.

These percentages are calculated live on your chart and updated after each period closes.

✅ Stats Table

A customizable on-chart table summarizing all of these stats in real-time.

Helps traders evaluate the effectiveness of range-based trading setups over time.

How it Works (Technical details)

On each new bar, the script checks if a new period (as defined by your timeframe selection) has begun.

When a new period starts, the previous period’s high, low, open, midline, quartiles are recorded and drawn on the chart.

The script then “watches” the current period:

Updates provisional high and low.

Detects sweeps of previous highs/lows.

Tracks if price returns to the previous period’s midline or open after those sweeps.

Increments statistical counters if conditions are met.

Background fills and lines update dynamically based on real-time data.

Intended Use Cases

This indicator is ideal for:

✅ Identifying premium/discount zones for swing or intraday trades.

✅ Spotting liquidity sweeps and possible manipulation zones.

✅ Structuring trades with logical, data-driven target zones (midline, open).

✅ Quantifying the probability of mean-reversion moves after liquidity events.

✅ Developing and backtesting range-based trading models with live stats.

Highly Customizable

Choose any timeframe for defining the premium/discount range.

Toggle visibility of midline, quartiles, open line, current period preview.

Full control over colors, line styles, line widths, and background shading.

Optional real-time statistical table with total counts and return percentages.

Swing High/Low with Liquidity Sweeps🧠 Overview

This indicator identifies swing highs and swing lows based on user-defined candle lengths and checks for liquidity sweeps—situations where the price breaks a previous swing level but then closes back inside, indicating a potential false breakout or stop hunt. It also supports visual labeling and alerts for these events.

⚙️ Inputs

Swing Length (must be odd number ≥ 3):

Determines how many candles are used to identify swing highs/lows. The central candle must be higher or lower than all neighbors within the range.

Example: If swingLength = 5, the central candle must be higher/lower than the 2 candles on both sides.

Sweep Lookback (bars):

Defines how many bars to look back for possible liquidity sweeps.

Show Swing Labels (checkbox):

Optionally display labels on the chart when a swing high or low is detected.

Show Sweep Labels (checkbox):

Optionally display labels on the chart when a liquidity sweep occurs.

🕯️ Swing Detection Logic

A Swing High is detected when the high of the central candle is greater than the highs of all candles around it (as per the defined length).

A Swing Low is detected when the low of the central candle is lower than the lows of surrounding candles.

Swing labels are placed slightly above (for highs) or below (for lows) the candle.

💧 Liquidity Sweep Logic

A Sweep High is triggered if:

The current high breaks above a previously detected swing high,

And then the candle closes below that swing high,

Within the configured lookback window.

A Sweep Low is triggered if:

The current low breaks below a previous swing low,

And then closes above it,

Within the lookback window.

These are often seen as stop hunts or fake breakouts.

🔔 Alerts

Sweep High Alert: Triggered when a sweep above a swing high occurs.

Sweep Low Alert: Triggered when a sweep below a swing low occurs.

You can use these to set up TradingView alerts to notify you of potential liquidity grabs.

📊 Use Cases

Identifying market structure shifts.

Spotting fake breakouts and potential reversals.

Assisting in smart money concepts and liquidity-based trading.

Supporting entry timing in trend continuation or reversal strategies.

Tensor Market Analysis Engine (TMAE)# Tensor Market Analysis Engine (TMAE)

## Advanced Multi-Dimensional Mathematical Analysis System

*Where Quantum Mathematics Meets Market Structure*

---

## 🎓 THEORETICAL FOUNDATION

The Tensor Market Analysis Engine represents a revolutionary synthesis of three cutting-edge mathematical frameworks that have never before been combined for comprehensive market analysis. This indicator transcends traditional technical analysis by implementing advanced mathematical concepts from quantum mechanics, information theory, and fractal geometry.

### 🌊 Multi-Dimensional Volatility with Jump Detection

**Hawkes Process Implementation:**

The TMAE employs a sophisticated Hawkes process approximation for detecting self-exciting market jumps. Unlike traditional volatility measures that treat price movements as independent events, the Hawkes process recognizes that market shocks cluster and exhibit memory effects.

**Mathematical Foundation:**

```

Intensity λ(t) = μ + Σ α(t - Tᵢ)

```

Where market jumps at times Tᵢ increase the probability of future jumps through the decay function α, controlled by the Hawkes Decay parameter (0.5-0.99).

**Mahalanobis Distance Calculation:**

The engine calculates volatility jumps using multi-dimensional Mahalanobis distance across up to 5 volatility dimensions:

- **Dimension 1:** Price volatility (standard deviation of returns)

- **Dimension 2:** Volume volatility (normalized volume fluctuations)

- **Dimension 3:** Range volatility (high-low spread variations)

- **Dimension 4:** Correlation volatility (price-volume relationship changes)

- **Dimension 5:** Microstructure volatility (intrabar positioning analysis)

This creates a volatility state vector that captures market behavior impossible to detect with traditional single-dimensional approaches.

### 📐 Hurst Exponent Regime Detection

**Fractal Market Hypothesis Integration:**

The TMAE implements advanced Rescaled Range (R/S) analysis to calculate the Hurst exponent in real-time, providing dynamic regime classification:

- **H > 0.6:** Trending (persistent) markets - momentum strategies optimal

- **H < 0.4:** Mean-reverting (anti-persistent) markets - contrarian strategies optimal

- **H ≈ 0.5:** Random walk markets - breakout strategies preferred

**Adaptive R/S Analysis:**

Unlike static implementations, the TMAE uses adaptive windowing that adjusts to market conditions:

```

H = log(R/S) / log(n)

```

Where R is the range of cumulative deviations and S is the standard deviation over period n.

**Dynamic Regime Classification:**

The system employs hysteresis to prevent regime flipping, requiring sustained Hurst values before regime changes are confirmed. This prevents false signals during transitional periods.

### 🔄 Transfer Entropy Analysis

**Information Flow Quantification:**

Transfer entropy measures the directional flow of information between price and volume, revealing lead-lag relationships that indicate future price movements:

```

TE(X→Y) = Σ p(yₜ₊₁, yₜ, xₜ) log

```

**Causality Detection:**

- **Volume → Price:** Indicates accumulation/distribution phases

- **Price → Volume:** Suggests retail participation or momentum chasing

- **Balanced Flow:** Market equilibrium or transition periods

The system analyzes multiple lag periods (2-20 bars) to capture both immediate and structural information flows.

---

## 🔧 COMPREHENSIVE INPUT SYSTEM

### Core Parameters Group

**Primary Analysis Window (10-100, Default: 50)**

The fundamental lookback period affecting all calculations. Optimization by timeframe:

- **1-5 minute charts:** 20-30 (rapid adaptation to micro-movements)

- **15 minute-1 hour:** 30-50 (balanced responsiveness and stability)

- **4 hour-daily:** 50-100 (smooth signals, reduced noise)

- **Asset-specific:** Cryptocurrency 20-35, Stocks 35-50, Forex 40-60

**Signal Sensitivity (0.1-2.0, Default: 0.7)**

Master control affecting all threshold calculations:

- **Conservative (0.3-0.6):** High-quality signals only, fewer false positives

- **Balanced (0.7-1.0):** Optimal risk-reward ratio for most trading styles

- **Aggressive (1.1-2.0):** Maximum signal frequency, requires careful filtering

**Signal Generation Mode:**

- **Aggressive:** Any component signals (highest frequency)

- **Confluence:** 2+ components agree (balanced approach)

- **Conservative:** All 3 components align (highest quality)

### Volatility Jump Detection Group

**Volatility Dimensions (2-5, Default: 3)**

Determines the mathematical space complexity:

- **2D:** Price + Volume volatility (suitable for clean markets)

- **3D:** + Range volatility (optimal for most conditions)

- **4D:** + Correlation volatility (advanced multi-asset analysis)

- **5D:** + Microstructure volatility (maximum sensitivity)

**Jump Detection Threshold (1.5-4.0σ, Default: 3.0σ)**

Standard deviations required for volatility jump classification:

- **Cryptocurrency:** 2.0-2.5σ (naturally volatile)

- **Stock Indices:** 2.5-3.0σ (moderate volatility)

- **Forex Major Pairs:** 3.0-3.5σ (typically stable)

- **Commodities:** 2.0-3.0σ (varies by commodity)

**Jump Clustering Decay (0.5-0.99, Default: 0.85)**

Hawkes process memory parameter:

- **0.5-0.7:** Fast decay (jumps treated as independent)

- **0.8-0.9:** Moderate clustering (realistic market behavior)

- **0.95-0.99:** Strong clustering (crisis/event-driven markets)

### Hurst Exponent Analysis Group

**Calculation Method Options:**

- **Classic R/S:** Original Rescaled Range (fast, simple)

- **Adaptive R/S:** Dynamic windowing (recommended for trading)

- **DFA:** Detrended Fluctuation Analysis (best for noisy data)

**Trending Threshold (0.55-0.8, Default: 0.60)**

Hurst value defining persistent market behavior:

- **0.55-0.60:** Weak trend persistence

- **0.65-0.70:** Clear trending behavior

- **0.75-0.80:** Strong momentum regimes

**Mean Reversion Threshold (0.2-0.45, Default: 0.40)**

Hurst value defining anti-persistent behavior:

- **0.35-0.45:** Weak mean reversion

- **0.25-0.35:** Clear ranging behavior

- **0.15-0.25:** Strong reversion tendency

### Transfer Entropy Parameters Group

**Information Flow Analysis:**

- **Price-Volume:** Classic flow analysis for accumulation/distribution

- **Price-Volatility:** Risk flow analysis for sentiment shifts

- **Multi-Timeframe:** Cross-timeframe causality detection

**Maximum Lag (2-20, Default: 5)**

Causality detection window:

- **2-5 bars:** Immediate causality (scalping)

- **5-10 bars:** Short-term flow (day trading)

- **10-20 bars:** Structural flow (swing trading)

**Significance Threshold (0.05-0.3, Default: 0.15)**

Minimum entropy for signal generation:

- **0.05-0.10:** Detect subtle information flows

- **0.10-0.20:** Clear causality only

- **0.20-0.30:** Very strong flows only

---

## 🎨 ADVANCED VISUAL SYSTEM

### Tensor Volatility Field Visualization

**Five-Layer Resonance Bands:**

The tensor field creates dynamic support/resistance zones that expand and contract based on mathematical field strength:

- **Core Layer (Purple):** Primary tensor field with highest intensity

- **Layer 2 (Neutral):** Secondary mathematical resonance

- **Layer 3 (Info Blue):** Tertiary harmonic frequencies

- **Layer 4 (Warning Gold):** Outer field boundaries

- **Layer 5 (Success Green):** Maximum field extension

**Field Strength Calculation:**

```

Field Strength = min(3.0, Mahalanobis Distance × Tensor Intensity)

```

The field amplitude adjusts to ATR and mathematical distance, creating dynamic zones that respond to market volatility.

**Radiation Line Network:**

During active tensor states, the system projects directional radiation lines showing field energy distribution:

- **8 Directional Rays:** Complete angular coverage

- **Tapering Segments:** Progressive transparency for natural visual flow

- **Pulse Effects:** Enhanced visualization during volatility jumps

### Dimensional Portal System

**Portal Mathematics:**

Dimensional portals visualize regime transitions using category theory principles:

- **Green Portals (◉):** Trending regime detection (appear below price for support)

- **Red Portals (◎):** Mean-reverting regime (appear above price for resistance)

- **Yellow Portals (○):** Random walk regime (neutral positioning)

**Tensor Trail Effects:**

Each portal generates 8 trailing particles showing mathematical momentum:

- **Large Particles (●):** Strong mathematical signal

- **Medium Particles (◦):** Moderate signal strength

- **Small Particles (·):** Weak signal continuation

- **Micro Particles (˙):** Signal dissipation

### Information Flow Streams

**Particle Stream Visualization:**

Transfer entropy creates flowing particle streams indicating information direction:

- **Upward Streams:** Volume leading price (accumulation phases)

- **Downward Streams:** Price leading volume (distribution phases)

- **Stream Density:** Proportional to information flow strength

**15-Particle Evolution:**

Each stream contains 15 particles with progressive sizing and transparency, creating natural flow visualization that makes information transfer immediately apparent.

### Fractal Matrix Grid System

**Multi-Timeframe Fractal Levels:**

The system calculates and displays fractal highs/lows across five Fibonacci periods:

- **8-Period:** Short-term fractal structure

- **13-Period:** Intermediate-term patterns

- **21-Period:** Primary swing levels

- **34-Period:** Major structural levels

- **55-Period:** Long-term fractal boundaries

**Triple-Layer Visualization:**

Each fractal level uses three-layer rendering:

- **Shadow Layer:** Widest, darkest foundation (width 5)

- **Glow Layer:** Medium white core line (width 3)

- **Tensor Layer:** Dotted mathematical overlay (width 1)

**Intelligent Labeling System:**

Smart spacing prevents label overlap using ATR-based minimum distances. Labels include:

- **Fractal Period:** Time-based identification

- **Topological Class:** Mathematical complexity rating (0, I, II, III)

- **Price Level:** Exact fractal price

- **Mahalanobis Distance:** Current mathematical field strength

- **Hurst Exponent:** Current regime classification

- **Anomaly Indicators:** Visual strength representations (○ ◐ ● ⚡)

### Wick Pressure Analysis

**Rejection Level Mathematics:**

The system analyzes candle wick patterns to project future pressure zones:

- **Upper Wick Analysis:** Identifies selling pressure and resistance zones

- **Lower Wick Analysis:** Identifies buying pressure and support zones

- **Pressure Projection:** Extends lines forward based on mathematical probability

**Multi-Layer Glow Effects:**

Wick pressure lines use progressive transparency (1-8 layers) creating natural glow effects that make pressure zones immediately visible without cluttering the chart.

### Enhanced Regime Background

**Dynamic Intensity Mapping:**

Background colors reflect mathematical regime strength:

- **Deep Transparency (98% alpha):** Subtle regime indication

- **Pulse Intensity:** Based on regime strength calculation

- **Color Coding:** Green (trending), Red (mean-reverting), Neutral (random)

**Smoothing Integration:**

Regime changes incorporate 10-bar smoothing to prevent background flicker while maintaining responsiveness to genuine regime shifts.

### Color Scheme System

**Six Professional Themes:**

- **Dark (Default):** Professional trading environment optimization

- **Light:** High ambient light conditions

- **Classic:** Traditional technical analysis appearance

- **Neon:** High-contrast visibility for active trading

- **Neutral:** Minimal distraction focus

- **Bright:** Maximum visibility for complex setups

Each theme maintains mathematical accuracy while optimizing visual clarity for different trading environments and personal preferences.

---

## 📊 INSTITUTIONAL-GRADE DASHBOARD

### Tensor Field Status Section

**Field Strength Display:**

Real-time Mahalanobis distance calculation with dynamic emoji indicators:

- **⚡ (Lightning):** Extreme field strength (>1.5× threshold)

- **● (Solid Circle):** Strong field activity (>1.0× threshold)

- **○ (Open Circle):** Normal field state

**Signal Quality Rating:**

Democratic algorithm assessment:

- **ELITE:** All 3 components aligned (highest probability)

- **STRONG:** 2 components aligned (good probability)

- **GOOD:** 1 component active (moderate probability)

- **WEAK:** No clear component signals

**Threshold and Anomaly Monitoring:**

- **Threshold Display:** Current mathematical threshold setting

- **Anomaly Level (0-100%):** Combined volatility and volume spike measurement

- **>70%:** High anomaly (red warning)

- **30-70%:** Moderate anomaly (orange caution)

- **<30%:** Normal conditions (green confirmation)

### Tensor State Analysis Section

**Mathematical State Classification:**

- **↑ BULL (Tensor State +1):** Trending regime with bullish bias

- **↓ BEAR (Tensor State -1):** Mean-reverting regime with bearish bias

- **◈ SUPER (Tensor State 0):** Random walk regime (neutral)

**Visual State Gauge:**

Five-circle progression showing tensor field polarity:

- **🟢🟢🟢⚪⚪:** Strong bullish mathematical alignment

- **⚪⚪🟡⚪⚪:** Neutral/transitional state

- **⚪⚪🔴🔴🔴:** Strong bearish mathematical alignment

**Trend Direction and Phase Analysis:**

- **📈 BULL / 📉 BEAR / ➡️ NEUTRAL:** Primary trend classification

- **🌪️ CHAOS:** Extreme information flow (>2.0 flow strength)

- **⚡ ACTIVE:** Strong information flow (1.0-2.0 flow strength)

- **😴 CALM:** Low information flow (<1.0 flow strength)

### Trading Signals Section

**Real-Time Signal Status:**

- **🟢 ACTIVE / ⚪ INACTIVE:** Long signal availability

- **🔴 ACTIVE / ⚪ INACTIVE:** Short signal availability

- **Components (X/3):** Active algorithmic components

- **Mode Display:** Current signal generation mode

**Signal Strength Visualization:**

Color-coded component count:

- **Green:** 3/3 components (maximum confidence)

- **Aqua:** 2/3 components (good confidence)

- **Orange:** 1/3 components (moderate confidence)

- **Gray:** 0/3 components (no signals)

### Performance Metrics Section

**Win Rate Monitoring:**

Estimated win rates based on signal quality with emoji indicators:

- **🔥 (Fire):** ≥60% estimated win rate

- **👍 (Thumbs Up):** 45-59% estimated win rate

- **⚠️ (Warning):** <45% estimated win rate

**Mathematical Metrics:**

- **Hurst Exponent:** Real-time fractal dimension (0.000-1.000)

- **Information Flow:** Volume/price leading indicators

- **📊 VOL:** Volume leading price (accumulation/distribution)

- **💰 PRICE:** Price leading volume (momentum/speculation)

- **➖ NONE:** Balanced information flow

- **Volatility Classification:**

- **🔥 HIGH:** Above 1.5× jump threshold

- **📊 NORM:** Normal volatility range

- **😴 LOW:** Below 0.5× jump threshold

### Market Structure Section (Large Dashboard)

**Regime Classification:**

- **📈 TREND:** Hurst >0.6, momentum strategies optimal

- **🔄 REVERT:** Hurst <0.4, contrarian strategies optimal

- **🎲 RANDOM:** Hurst ≈0.5, breakout strategies preferred

**Mathematical Field Analysis:**

- **Dimensions:** Current volatility space complexity (2D-5D)

- **Hawkes λ (Lambda):** Self-exciting jump intensity (0.00-1.00)

- **Jump Status:** 🚨 JUMP (active) / ✅ NORM (normal)

### Settings Summary Section (Large Dashboard)

**Active Configuration Display:**

- **Sensitivity:** Current master sensitivity setting

- **Lookback:** Primary analysis window

- **Theme:** Active color scheme

- **Method:** Hurst calculation method (Classic R/S, Adaptive R/S, DFA)

**Dashboard Sizing Options:**

- **Small:** Essential metrics only (mobile/small screens)

- **Normal:** Balanced information density (standard desktop)

- **Large:** Maximum detail (multi-monitor setups)

**Position Options:**

- **Top Right:** Standard placement (avoids price action)

- **Top Left:** Wide chart optimization

- **Bottom Right:** Recent price focus (scalping)

- **Bottom Left:** Maximum price visibility (swing trading)

---

## 🎯 SIGNAL GENERATION LOGIC

### Multi-Component Convergence System

**Component Signal Architecture:**

The TMAE generates signals through sophisticated component analysis rather than simple threshold crossing:

**Volatility Component:**

- **Jump Detection:** Mahalanobis distance threshold breach

- **Hawkes Intensity:** Self-exciting process activation (>0.2)

- **Multi-dimensional:** Considers all volatility dimensions simultaneously

**Hurst Regime Component:**

- **Trending Markets:** Price above SMA-20 with positive momentum

- **Mean-Reverting Markets:** Price at Bollinger Band extremes

- **Random Markets:** Bollinger squeeze breakouts with directional confirmation

**Transfer Entropy Component:**

- **Volume Leadership:** Information flow from volume to price

- **Volume Spike:** Volume 110%+ above 20-period average

- **Flow Significance:** Above entropy threshold with directional bias

### Democratic Signal Weighting

**Signal Mode Implementation:**

- **Aggressive Mode:** Any single component triggers signal

- **Confluence Mode:** Minimum 2 components must agree

- **Conservative Mode:** All 3 components must align

**Momentum Confirmation:**

All signals require momentum confirmation:

- **Long Signals:** RSI >50 AND price >EMA-9

- **Short Signals:** RSI <50 AND price 0.6):**

- **Increase Sensitivity:** Catch momentum continuation

- **Lower Mean Reversion Threshold:** Avoid counter-trend signals

- **Emphasize Volume Leadership:** Institutional accumulation/distribution

- **Tensor Field Focus:** Use expansion for trend continuation

- **Signal Mode:** Aggressive or Confluence for trend following

**Range-Bound Markets (Hurst <0.4):**

- **Decrease Sensitivity:** Avoid false breakouts

- **Lower Trending Threshold:** Quick regime recognition

- **Focus on Price Leadership:** Retail sentiment extremes

- **Fractal Grid Emphasis:** Support/resistance trading

- **Signal Mode:** Conservative for high-probability reversals

**Volatile Markets (High Jump Frequency):**

- **Increase Hawkes Decay:** Recognize event clustering

- **Higher Jump Threshold:** Avoid noise signals

- **Maximum Dimensions:** Capture full volatility complexity

- **Reduce Position Sizing:** Risk management adaptation

- **Enhanced Visuals:** Maximum information for rapid decisions

**Low Volatility Markets (Low Jump Frequency):**

- **Decrease Jump Threshold:** Capture subtle movements

- **Lower Hawkes Decay:** Treat moves as independent

- **Reduce Dimensions:** Simplify analysis

- **Increase Position Sizing:** Capitalize on compressed volatility

- **Minimal Visuals:** Reduce distraction in quiet markets

---

## 🚀 ADVANCED TRADING STRATEGIES

### The Mathematical Convergence Method

**Entry Protocol:**

1. **Fractal Grid Approach:** Monitor price approaching significant fractal levels

2. **Tensor Field Confirmation:** Verify field expansion supporting direction

3. **Portal Signal:** Wait for dimensional portal appearance

4. **ELITE/STRONG Quality:** Only trade highest quality mathematical signals

5. **Component Consensus:** Confirm 2+ components agree in Confluence mode

**Example Implementation:**

- Price approaching 21-period fractal high

- Tensor field expanding upward (bullish mathematical alignment)

- Green portal appears below price (trending regime confirmation)

- ELITE quality signal with 3/3 components active

- Enter long position with stop below fractal level

**Risk Management:**

- **Stop Placement:** Below/above fractal level that generated signal

- **Position Sizing:** Based on Mahalanobis distance (higher distance = smaller size)

- **Profit Targets:** Next fractal level or tensor field resistance

### The Regime Transition Strategy

**Regime Change Detection:**

1. **Monitor Hurst Exponent:** Watch for persistent moves above/below thresholds

2. **Portal Color Change:** Regime transitions show different portal colors

3. **Background Intensity:** Increasing regime background intensity

4. **Mathematical Confirmation:** Wait for regime confirmation (hysteresis)

**Trading Implementation:**

- **Trending Transitions:** Trade momentum breakouts, follow trend

- **Mean Reversion Transitions:** Trade range boundaries, fade extremes

- **Random Transitions:** Trade breakouts with tight stops

**Advanced Techniques:**

- **Multi-Timeframe:** Confirm regime on higher timeframe

- **Early Entry:** Enter on regime transition rather than confirmation

- **Regime Strength:** Larger positions during strong regime signals

### The Information Flow Momentum Strategy

**Flow Detection Protocol:**

1. **Monitor Transfer Entropy:** Watch for significant information flow shifts

2. **Volume Leadership:** Strong edge when volume leads price

3. **Flow Acceleration:** Increasing flow strength indicates momentum

4. **Directional Confirmation:** Ensure flow aligns with intended trade direction

**Entry Signals:**

- **Volume → Price Flow:** Enter during accumulation/distribution phases

- **Price → Volume Flow:** Enter on momentum confirmation breaks

- **Flow Reversal:** Counter-trend entries when flow reverses

**Optimization:**

- **Scalping:** Use immediate flow detection (2-5 bar lag)

- **Swing Trading:** Use structural flow (10-20 bar lag)

- **Multi-Asset:** Compare flow between correlated assets

### The Tensor Field Expansion Strategy

**Field Mathematics:**

The tensor field expansion indicates mathematical pressure building in market structure:

**Expansion Phases:**

1. **Compression:** Field contracts, volatility decreases

2. **Tension Building:** Mathematical pressure accumulates

3. **Expansion:** Field expands rapidly with directional movement

4. **Resolution:** Field stabilizes at new equilibrium

**Trading Applications:**

- **Compression Trading:** Prepare for breakout during field contraction

- **Expansion Following:** Trade direction of field expansion

- **Reversion Trading:** Fade extreme field expansion

- **Multi-Dimensional:** Consider all field layers for confirmation

### The Hawkes Process Event Strategy

**Self-Exciting Jump Trading:**

Understanding that market shocks cluster and create follow-on opportunities:

**Jump Sequence Analysis:**

1. **Initial Jump:** First volatility jump detected

2. **Clustering Phase:** Hawkes intensity remains elevated

3. **Follow-On Opportunities:** Additional jumps more likely

4. **Decay Period:** Intensity gradually decreases

**Implementation:**

- **Jump Confirmation:** Wait for mathematical jump confirmation

- **Direction Assessment:** Use other components for direction

- **Clustering Trades:** Trade subsequent moves during high intensity

- **Decay Exit:** Exit positions as Hawkes intensity decays

### The Fractal Confluence System

**Multi-Timeframe Fractal Analysis:**

Combining fractal levels across different periods for high-probability zones:

**Confluence Zones:**

- **Double Confluence:** 2 fractal levels align

- **Triple Confluence:** 3+ fractal levels cluster

- **Mathematical Confirmation:** Tensor field supports the level

- **Information Flow:** Transfer entropy confirms direction

**Trading Protocol:**

1. **Identify Confluence:** Find 2+ fractal levels within 1 ATR

2. **Mathematical Support:** Verify tensor field alignment

3. **Signal Quality:** Wait for STRONG or ELITE signal

4. **Risk Definition:** Use fractal level for stop placement

5. **Profit Targeting:** Next major fractal confluence zone

---

## ⚠️ COMPREHENSIVE RISK MANAGEMENT

### Mathematical Position Sizing

**Mahalanobis Distance Integration:**

Position size should inversely correlate with mathematical field strength:

```

Position Size = Base Size × (Threshold / Mahalanobis Distance)

```

**Risk Scaling Matrix:**

- **Low Field Strength (<2.0):** Standard position sizing

- **Moderate Field Strength (2.0-3.0):** 75% position sizing

- **High Field Strength (3.0-4.0):** 50% position sizing

- **Extreme Field Strength (>4.0):** 25% position sizing or no trade

### Signal Quality Risk Adjustment

**Quality-Based Position Sizing:**

- **ELITE Signals:** 100% of planned position size

- **STRONG Signals:** 75% of planned position size

- **GOOD Signals:** 50% of planned position size

- **WEAK Signals:** No position or paper trading only

**Component Agreement Scaling:**

- **3/3 Components:** Full position size

- **2/3 Components:** 75% position size

- **1/3 Components:** 50% position size or skip trade

### Regime-Adaptive Risk Management

**Trending Market Risk:**

- **Wider Stops:** Allow for trend continuation

- **Trend Following:** Trade with regime direction

- **Higher Position Size:** Trend probability advantage

- **Momentum Stops:** Trail stops based on momentum indicators

**Mean-Reverting Market Risk:**

- **Tighter Stops:** Quick exits on trend continuation

- **Contrarian Positioning:** Trade against extremes

- **Smaller Position Size:** Higher reversal failure rate

- **Level-Based Stops:** Use fractal levels for stops

**Random Market Risk:**

- **Breakout Focus:** Trade only clear breakouts

- **Tight Initial Stops:** Quick exit if breakout fails

- **Reduced Frequency:** Skip marginal setups

- **Range-Based Targets:** Profit targets at range boundaries

### Volatility-Adaptive Risk Controls

**High Volatility Periods:**

- **Reduced Position Size:** Account for wider price swings

- **Wider Stops:** Avoid noise-based exits

- **Lower Frequency:** Skip marginal setups

- **Faster Exits:** Take profits more quickly

**Low Volatility Periods:**

- **Standard Position Size:** Normal risk parameters

- **Tighter Stops:** Take advantage of compressed ranges

- **Higher Frequency:** Trade more setups

- **Extended Targets:** Allow for compressed volatility expansion

### Multi-Timeframe Risk Alignment

**Higher Timeframe Trend:**

- **With Trend:** Standard or increased position size

- **Against Trend:** Reduced position size or skip

- **Neutral Trend:** Standard position size with tight management

**Risk Hierarchy:**

1. **Primary:** Current timeframe signal quality

2. **Secondary:** Higher timeframe trend alignment

3. **Tertiary:** Mathematical field strength

4. **Quaternary:** Market regime classification

---

## 📚 EDUCATIONAL VALUE AND MATHEMATICAL CONCEPTS

### Advanced Mathematical Concepts

**Tensor Analysis in Markets:**

The TMAE introduces traders to tensor analysis, a branch of mathematics typically reserved for physics and advanced engineering. Tensors provide a framework for understanding multi-dimensional market relationships that scalar and vector analysis cannot capture.

**Information Theory Applications:**

Transfer entropy implementation teaches traders about information flow in markets, a concept from information theory that quantifies directional causality between variables. This provides intuition about market microstructure and participant behavior.

**Fractal Geometry in Trading:**

The Hurst exponent calculation exposes traders to fractal geometry concepts, helping understand that markets exhibit self-similar patterns across multiple timeframes. This mathematical insight transforms how traders view market structure.

**Stochastic Process Theory:**

The Hawkes process implementation introduces concepts from stochastic process theory, specifically self-exciting point processes. This provides mathematical framework for understanding why market events cluster and exhibit memory effects.

### Learning Progressive Complexity

**Beginner Mathematical Concepts:**

- **Volatility Dimensions:** Understanding multi-dimensional analysis

- **Regime Classification:** Learning market personality types

- **Signal Democracy:** Algorithmic consensus building

- **Visual Mathematics:** Interpreting mathematical concepts visually

**Intermediate Mathematical Applications:**

- **Mahalanobis Distance:** Statistical distance in multi-dimensional space

- **Rescaled Range Analysis:** Fractal dimension measurement

- **Information Entropy:** Quantifying uncertainty and causality

- **Field Theory:** Understanding mathematical fields in market context

**Advanced Mathematical Integration:**

- **Tensor Field Dynamics:** Multi-dimensional market force analysis

- **Stochastic Self-Excitation:** Event clustering and memory effects

- **Categorical Composition:** Mathematical signal combination theory

- **Topological Market Analysis:** Understanding market shape and connectivity

### Practical Mathematical Intuition

**Developing Market Mathematics Intuition:**

The TMAE serves as a bridge between abstract mathematical concepts and practical trading applications. Traders develop intuitive understanding of:

- **How markets exhibit mathematical structure beneath apparent randomness**

- **Why multi-dimensional analysis reveals patterns invisible to single-variable approaches**

- **How information flows through markets in measurable, predictable ways**

- **Why mathematical models provide probabilistic edges rather than certainties**

---

## 🔬 IMPLEMENTATION AND OPTIMIZATION

### Getting Started Protocol

**Phase 1: Observation (Week 1)**

1. **Apply with defaults:** Use standard settings on your primary trading timeframe

2. **Study visual elements:** Learn to interpret tensor fields, portals, and streams

3. **Monitor dashboard:** Observe how metrics change with market conditions

4. **No trading:** Focus entirely on pattern recognition and understanding

**Phase 2: Pattern Recognition (Week 2-3)**

1. **Identify signal patterns:** Note what market conditions produce different signal qualities

2. **Regime correlation:** Observe how Hurst regimes affect signal performance

3. **Visual confirmation:** Learn to read tensor field expansion and portal signals

4. **Component analysis:** Understand which components drive signals in different markets

**Phase 3: Parameter Optimization (Week 4-5)**

1. **Asset-specific tuning:** Adjust parameters for your specific trading instrument

2. **Timeframe optimization:** Fine-tune for your preferred trading timeframe

3. **Sensitivity adjustment:** Balance signal frequency with quality

4. **Visual customization:** Optimize colors and intensity for your trading environment

**Phase 4: Live Implementation (Week 6+)**

1. **Paper trading:** Test signals with hypothetical trades

2. **Small position sizing:** Begin with minimal risk during learning phase

3. **Performance tracking:** Monitor actual vs. expected signal performance